AI in Commercial Real Estate

April 29, 2026

AI in Commercial Real Estate

April 29, 2026

Two years ago, generative AI in commercial real estate lending was a conference topic. Today, it is operational infrastructure. According to JLL's 2025 Global Real Estate Technology Survey, 88% of CRE investors, owners, and landlords have started piloting AI — up from just 5% three years earlier — yet only 5% report that they are actually achieving their stated AI objectives. The gap between piloting and operating is now where competitive advantage in CRE lending is decided.

This article distills what Smart Capital Center presented at the MBA Servicing Conference on the role of generative AI in CRE lending and asset management — and updates each section with the data, deployments, and regulatory context that have emerged since.

Most CRE writeups still reference the "BCG study" loosely. The primary source is Navigating the Jagged Technological Frontier, a 2023 Harvard Business School working paper authored with researchers from MIT, Wharton, Warwick, and BCG.

In a controlled study of 758 BCG consultants across 18 realistic tasks, those using GPT-4 completed 12.2% more tasks, worked 25.1% faster, and produced output rated 40% higher in quality by human evaluators. Critically, the lowest performers gained the most — a 43% improvement versus 17% for top performers — meaning AI compresses the productivity gap inside teams, not just lifts the average.

The applied lesson for CRE lenders: AI doesn't replace senior credit officers; it raises the floor for analysts, associates, and outsourced support so that senior judgment is the bottleneck again — not data processing.

The most consequential change since the MBA Servicing Conference is the transition from AI assistants (which respond to a single prompt) to AI agents (which orchestrate multi-step workflows autonomously).

McKinsey's 2026 analysis of agentic AI in real estate frames it directly: the shift is "from 'help me understand' to 'help me get it done.'" The firm estimates agentic automation could unlock $430–$550 billion in annual value across real estate, construction, and development globally.

In CRE lending specifically, that means agents now:

The regulatory environment is hardening to match. The EU AI Act entered full enforcement for high-risk AI systems in financial services in August 2026, formalizing requirements for explainability, bias auditing, and human-in-the-loop oversight. U.S. institutions serving EU borrowers — or operating in jurisdictions modeling EU rules — face equivalent pressure.

"The shift is from 'help me understand' to 'help me get it done.' Although deploying agentic systems successfully is challenging, the potential value is enormous." — McKinsey & Company, How Agentic AI in Real Estate Can Automate Workflows (March 2026)

Generative AI now operates across every stage of CRE lending and servicing. The applications below are deployed in production at Smart Capital Center and across the platforms tracked in the CBRE 2025 Tech Adoption Report, which found that development and credit teams using AI for underwriting complete preliminary analysis approximately 3x faster than teams without it.

Generative AI summarizes deal memos, market reports, leases, loan agreements, and OMs with a level of accuracy that depends almost entirely on prompt design. Strong summarization workflows use structured templates, role-conditioned prompts, and grounding against a verified document corpus. Personalization (audience, length, level of technicality) further improves output quality.

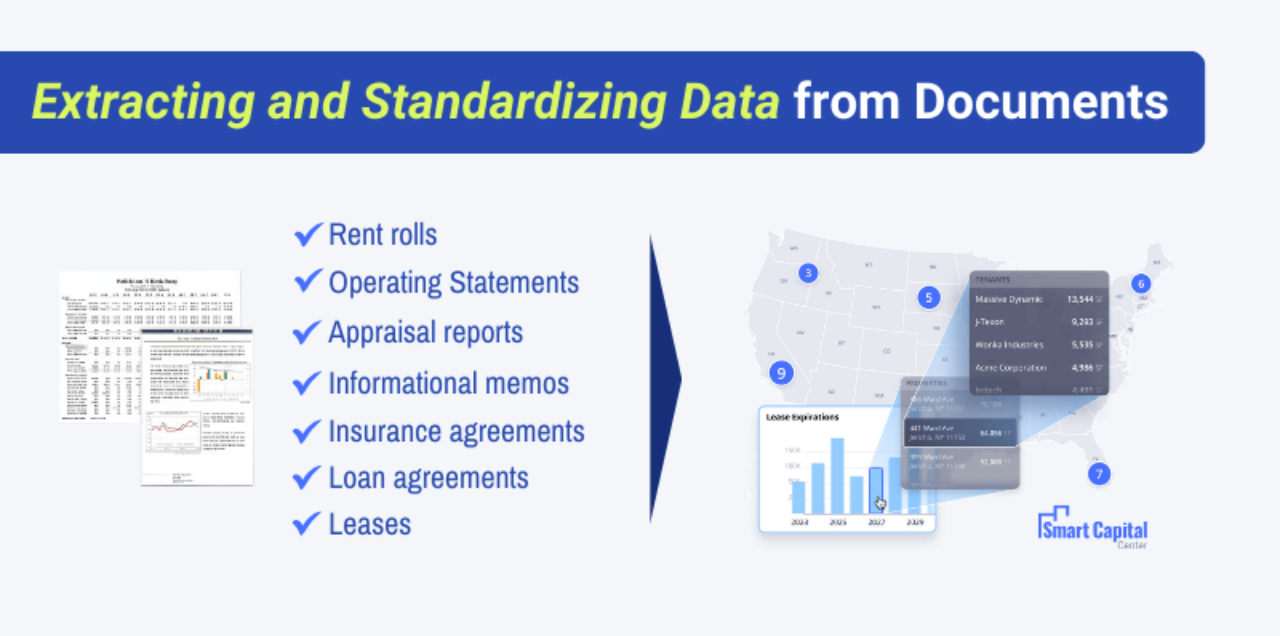

AI accelerates tenant credit screening, market comp pulling, deal-risk identification, and zoning or regulatory summarization. Smart Capital Center's research module pulls live data across 120M+ properties and synthesizes risk flags in seconds rather than the multi-day cycles typical of traditional research processes.

Rent rolls, T-12s, and operating statements arrive in dozens of formats — PDF, scanned image, Excel, CSV. AI-powered extraction normalizes these into structured data ready for variance analysis, normalization, and downstream financial modeling. This is the foundation that all subsequent automation depends on.

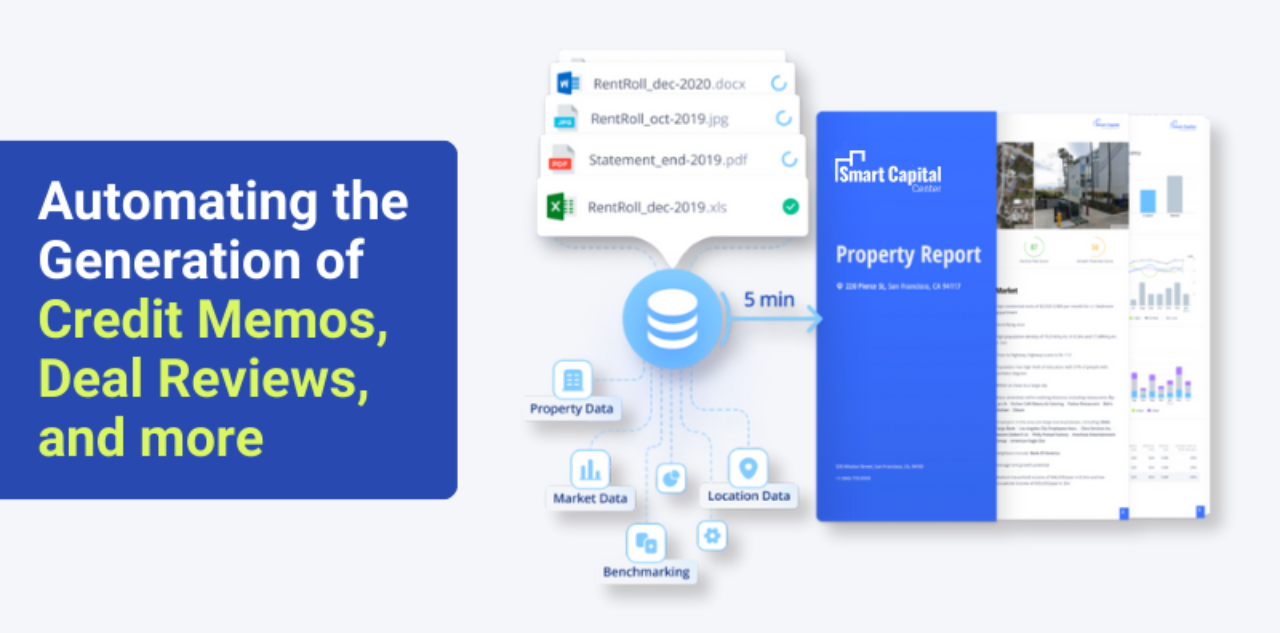

Once data is structured, AI generates charts, comparison tables, and visualizations on demand — in plain language, without SQL or BI configuration. The user describes the chart they want; the system produces it. This compresses the time between question and answer in investment committee discussions.

AI now generates first-draft credit memos, including borrower summaries, financial analysis sections, market commentary, and preliminary risk assessments. Senior credit officers review and refine rather than draft from scratch. According to EY, agentic AI can reduce the time spent on manual AML and KYC investigations by 50% by reasoning through complex ownership structures and producing auditable memos.

AI-generated alerts, deal-team notes, and borrower communications standardize tone and ensure nothing falls through the cracks. Smart Capital Center's borrower portal generates personalized notifications, payment reminders, and document-request follow-ups automatically.

Goldman Sachs estimated in mid-2025 that AI tools could reduce CRE due diligence costs by 20% to 35% for large institutional portfolios. The savings concentrate in three places:

The platforms capturing this value are the ones running agentic orchestration end-to-end, not those bolting a chatbot onto a legacy system.

The risks discussed at the MBA Servicing Conference still apply — and have sharpened with regulatory enforcement.

The impact on the future of CRE work

The labor implications are clearer in 2026 than they were at the conference. Three patterns have crystallized:

JLL CTO Yao Morin summarized the divide: "Companies investing early in strong data platforms are now leading the way. A robust data foundation is essential for growth, and organizations preparing for advanced AI applications will continue to gain momentum and stay ahead of the competition."

Smart Capital Center is an AI-powered underwriting, portfolio insight, and debt management platform used by KeyBank, JLL, RGA, Pacific Life, The RMR Group, and other leading institutional investors and lenders. The platform was named a GlobeSt Influencer in CRE Technology in both 2024 and 2026.

For CRE lenders and servicers, the platform delivers:

For a deeper look, see our recap of MBA CREF 2024 takeaways and our two-part series on the future role of generative AI in CRE lending.

What is agentic AI, and how does it differ from generative AI in CRE lending?

Generative AI produces output in response to a prompt — a summary, a draft memo, a chart. Agentic AI orchestrates multi-step workflows autonomously: pulling data, running models, flagging anomalies, and routing exceptions without human handoffs at each step. According to McKinsey, the shift from generative to agentic represents the difference between "help me understand" and "help me get it done," and could unlock $430–$550 billion in annual value across real estate, construction, and development globally.

How much faster is AI-augmented CRE underwriting?

According to the CBRE 2025 Tech Adoption Report, development and credit teams using AI for underwriting complete preliminary analysis approximately 3x faster than teams without it. Goldman Sachs estimated in 2025 that AI tools could reduce overall CRE due diligence costs by 20% to 35% for large institutional portfolios. Smart Capital Center clients typically see deal-underwriting cycle times compressed from days to minutes for standard multifamily and commercial deals.

What productivity gains has AI delivered in knowledge work?

The Harvard / BCG / MIT / Wharton / Warwick Navigating the Jagged Technological Frontier study found that consultants using GPT-4 completed 12.2% more tasks, worked 25.1% faster, and produced output rated 40% higher in quality. The largest gains went to lower performers (43%) versus top performers (17%), demonstrating AI's role as a skill leveler.

What are the main risks of using AI in CRE lending?

The five primary risks are reliability (hallucinations on financial data), data privacy (borrower and tenant information), bias (fair-lending compliance), cost (integration and ongoing infrastructure), and regulation. The EU AI Act entered full enforcement for high-risk AI in financial services in August 2026, and U.S. regulators (OCC, FDIC, CFPB) have issued model-risk guidance specific to AI. Mature CRE platforms address these through grounding, private model instances, bias auditing, and structured human-in-the-loop review.

Will AI replace human credit officers and underwriters?

No. AI replaces analytical and document-processing tasks within underwriting and servicing, but credit judgment, structuring, and borrower relationships remain human work. The pattern emerging in 2026 is hybrid teams: AI handles ingestion, normalization, modeling, and first-draft documentation; humans focus on judgment-intensive decisions, exception handling, and client relationships.

How does Smart Capital Center help lenders and servicers operationalize AI?

Smart Capital Center provides production-ready AI for CRE underwriting, portfolio monitoring, and debt management — already integrated with the data sources, document formats, and reporting systems used by institutional lenders. The platform analyzes 1B+ real-time data points across 120M+ properties, has supported $500B+ in CRE transactions, and integrates with Yardi, ARGUS, SS&C Precision, and Midland Enterprise via API. Book a demo to see it applied to your loan book.

Move faster. Finance smarter. Outperform at scale. Smart Capital Center turns fragmented loan and portfolio data into faster underwriting, sharper risk insight, and lower servicing costs. Book a demo today.

Or request a copy of our Generative AI in CRE Lending and Servicing brochure at demo@smartcapital.center.

.png)