AI in Commercial Real Estate

June 16, 2026

AI in Commercial Real Estate

June 16, 2026

According to Deloitte's 2026 Commercial Real Estate Outlook, surveying over 850 C-suite executives at firms managing more than $250 million in assets, 81% of global CRE leaders expect generative AI to materially reshape their business within three years — yet only 9% report that their organizations have fully operationalized GenAI across the lending and asset management lifecycle. The gap between intent and execution is where the next wave of competitive separation in CRE finance will be decided.

In Part 1 of this serie we covered the foundations of generative AI, the underlying transformer technology, and where it is already affecting productivity in CRE finance today. This second part maps exactly where generative AI changes the lending and asset management workflow — from due diligence through closing through portfolio monitoring — and what the measurable impact looks like in practice.

This analysis draws on Smart Capital Center — a CRE AI platform that has processed $500B+ in transactions across 120M+ properties, used by JLL, KeyBank, and leading institutional lenders — to show what generative AI in CRE lending actually delivers when deployed end-to-end.

The due-diligence process in real estate transactions is a cornerstone of sound investment decisions. This traditionally labor-intensive task, requiring detailed examination of extensive documentation, can now be significantly streamlined with the introduction of Generative AI.

Leases define the cash flow that supports every income-producing CRE asset. A misread escalation clause, missed co-tenancy provision, or overlooked option period can change a deal's underwritten NOI by 5–15% — and the error rarely surfaces until well after closing.

Generative AI assists lease analysis by:

"What used to take 30 to 40 minutes per financial statement now takes one to three minutes — and the output goes directly into the model without a manual transfer step," said a Director of Asset Management at JLL. "We've seen a 90%+ reduction in the time spent on financial analysis, which lets the team focus on the work that actually requires judgment."

Insurance documents are dense, structurally inconsistent, and easy to under-review at the deal stage. A coverage gap or sub-limit issue identified post-closing becomes a borrower remediation requirement that delays funding and irritates relationships.

AI-powered insurance review identifies:

The output is a structured summary that allows a credit analyst to confirm coverage adequacy in 10–15 minutes rather than 90 minutes — a difference that compounds across the multiple insurance documents a typical loan package contains.

Beyond leases and insurance, CRE deals routinely involve partnership agreements, joint ventures, mortgages, ground leases, easements, and service contracts. Each carries its own provisions that can affect cash flow, ownership rights, or future liability.

Generative AI applied to legal documents:

For lenders and asset managers operating with limited internal legal capacity, AI-assisted legal review extends the depth of analysis the deal team can apply without increasing legal spend per transaction.

The credit memo is the document that moves a loan from underwriting to committee approval. Traditional preparation involves an analyst pulling data from multiple systems — accounting platforms, rent roll exports, market data subscriptions, internal benchmarking files — and assembling a structured narrative with financial analysis, risk identification, and mitigant discussion.

Most lenders still build credit memos largely by hand. The half-day to full-day drafting cycle is one of the most common bottlenecks in CRE lending pipelines.

Generative AI simplifies this work across three layers:

Data aggregation. AI pulls together the inputs required for a comprehensive credit analysis: borrower financial history, property-level performance data, market comparables, and tenant credit signals. Where an analyst previously spent two to four hours collecting and formatting data, an AI-powered platform delivers the structured inputs in minutes.

Risk analysis. Generative AI evaluates risk factors by analyzing patterns and anomalies across the deal data. Income volatility, occupancy variability, expense ratio outliers, and tenant concentration trends that might require an experienced underwriter several hours to surface are flagged automatically with the supporting evidence linked.

Financial modeling. AI-powered platforms generate financial models that project future performance under multiple scenarios. Machine learning processes large datasets — historical comparables, current market signals, and macroeconomic conditions — to build predictive models that account for variables like interest rate sensitivity, cap rate expansion, and vacancy stress.

These models deliver scenario analyses that stress-test financial assumptions by changing key inputs (occupancy, financing costs, expense growth) and show how the asset performs under each condition. They calculate the financial ratios lenders rely on:

Automated Valuation Models (AVMs) generated by AI provide rapid property valuations by analyzing comparable sales, property characteristics, and current market signals. When AVM outputs feed directly into the underwriting model, the time from document upload to a committee-ready package compresses from days to hours.

"By mid-implementation we had already cut the time to prepare financial models for loans by 40%," noted a Senior Vice President at KeyBank. "The data layer is current, it's traceable, and it holds up in credit review — which is what matters when the committee is looking at provenance."

Generative AI is not only redefining the backend of financial services but also transforming interactions between borrowers and lenders. By facilitating fast, effective communications, AI makes the loan process more transparent and efficient.

Streamlined Communication and Collaboration

Generative AI also excels in creating fast, informative, and well-written materials that bridge the communication gap between borrowers and lenders. This includes automatic generation of notes, messages, emails, documents, and chat Q&As, ensuring that all parties are consistently informed and engaged throughout the lending process.

By harnessing the power of AI, financial institutions can provide personalized and precise information tailored to the specific needs of each borrower, facilitating a smoother and more user-friendly experience.

Deal team members, including borrowers and lender deal team, can also be assigned various tasks, with the system sending out reminders and notifications, reducing the need for manual follow-ups. Generative AI helps streamline these processes with automated natural language messaging and reminders.

AI can prioritize tasks, suggest actions based on the data reviewed, and flag any issues or missing documents, ensuring nothing falls through the cracks.

Investor Portal and Borrower Engagement

A rich investor portal integrated with generative AI provides deep property and market insights, which not only drive engagement from borrowers but also strengthen relationships with the lender. The portal can serve personalized content, reports, and analytics to borrowers, keeping them informed and connected to the lender. This level of engagement is essential for building trust and fostering long-term partnerships.

Smart Capital is a great example of such digital space between property investors, lenders, and brokers. In addition to loan statements, document exchange, and messaging, the platform assists with routine tasks and helps each focus on critical decision-making.

By leveraging AI-powered platforms, such as Smart Capital Center, the digital workspace between lender and borrower can be transformed into a dynamic, interactive environment that not only enhances the efficiency of the lending process but also contributes to better customer service and stickier, stronger relationships between borrowers and lenders.

In the complex world of real estate, the volume and intricacy of deal-related documentation have grown substantially. For lenders and asset managers, GenAI is proving to be a game-changer, transforming the document creation process by leveraging its advanced understanding of language and context.

Optimized Loan Materials Preparation

The preparation of critical loan documents such as Letters of Intent (LOI), mortgage agreements, and other related notes and materials can be significantly enhanced with the adoption of Generative AI technology. This optimization not only speeds up the creation process but also improves the overall quality of these documents.

By automating and refining the drafting of such intricate paperwork, AI can reduce manual errors, ensure compliance with relevant regulations, and tailor each document to the specific needs of the transaction, leading to a more streamlined, efficient, and reliable loan materials preparation workflow.

In real estate, where document accuracy and persuasiveness are key, generative AI offers a significant advantage. It enables professionals to create high-quality documents more quickly and efficiently than traditional methods.

Data security has been a significant concern for many companies regarding the use of ChatGPT and similar LLMs. The apprehension about data leakage and privacy breaches has led to some organizations imposing bans on the use of these AI tools. However, the landscape of AI and data security is rapidly evolving, and these prohibitions are likely temporary. There are several reasons to be optimistic about the integration of LLMs into corporate environments:

Smart Capital Center's state-of-the-art technology excels at extracting and standardizing data from core documents. As a result, after such processing, Smart Capital can feed only selected data feeds to generative AI. For example, in analyzing rent rolls, Smart Capital Center first processes the documents internally, leveraging its own advanced technology. Afterward, the processed and carefully curated data feed, which excludes tenant names, property addresses, and any other identifying information, , is fed to an LLM. This method ensures that the LLM can still process and analyze relevant data without compromising privacy.

Given these developments, companies should consider transitioning from blanket bans on using Generative AI to targeted policies focusing on specific types of AI use. Such policies would enable corporations to leverage the benefits of AI while maintaining rigorous data security standards. As AI technology advances, its incorporation into corporate workflows is likely to become more secure and compliant with industry-specific regulations.

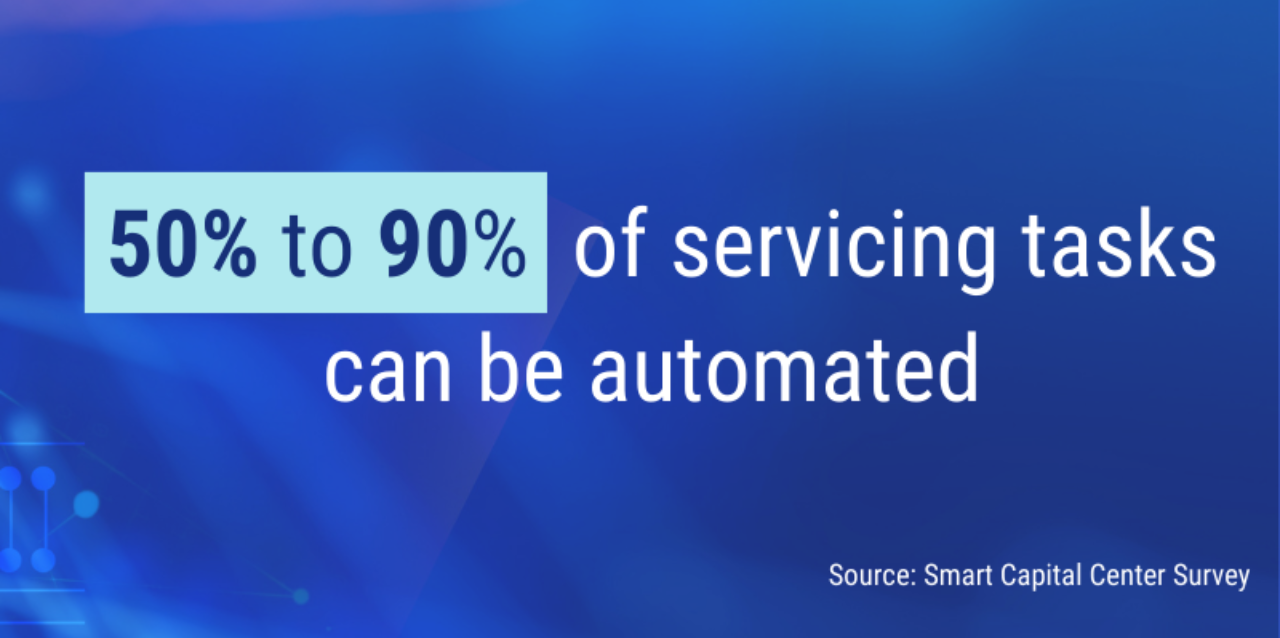

A survey by the Smart Capital Center team has uncovered a significant potential for automation in real estate servicing and asset management. Respondents estimate that between 50% to 90% of servicing tasks can be automated. This trend points towards a transformative shift in the industry, driven by the capabilities of AI.

Generative AI has been instrumental in automating financial analysis and providing deep portfolio insights. The AI system takes over the meticulous task of analyzing financial data, thereby offering real-time portfolio performance insights.

It also generates detailed financial commentaries, converting complex data into understandable and actionable insights.

In workflow automation, AI has shown significant efficiency, especially in areas such as draw management. It simplifies the process of managing fund flows and resource allocation.

The role of AI in processing invoices and reconciliation of expenses with budgets ensures accurate financial tracking and efficient construction loan management. The draw approval process is another area where AI-driven automation streamlines operations, enabling faster and more informed decisions.

Moreover, the role of GenAI in loan servicing extends to the meticulous monitoring of loans for compliance with terms and covenants, as well as proactive management of covenant-related metrics. The technology’s advanced algorithms can analyze compliance data, flag potential issues, and assist in maintaining covenant adherence, thereby enhancing risk management.

The survey findings underscore the growing importance of AI in real estate servicing and asset management. By automating a vast range of tasks, AI-powered platforms such as Smart Capital is not just enhancing operational efficiency but are also reshaping how financial analysis and portfolio management are conducted in the industry.

The finalization of loan transactions is a critical phase that has been significantly streamlined by the introduction of AI. This advanced system plays a pivotal role in ensuring that the transition to loan servicing is smooth and efficient.

Verifying Legal and Financial Documents

One of the key functions of LLM technology in loan closing is its ability to ensure that all necessary legal and financial documents are correctly completed, duly signed, and properly filed.

Efficient Document Cross-Verification and Closure Process

Traditionally, the process of cross-verifying documents and finalizing closing statements in CRE lending is time-consuming, often stretching over several weeks. LLM technology transforms this process by bringing in unparalleled efficiency.

Helping commercial real estate lenders and investors drive faster, more cost-efficient, and smarter financing processes and asset management is at the heart of Smart Capital Center's mission, a commitment further solidified by our integration of Generative AI into the platform. This advancement was prominently featured in our recent collaboration with top US Commercial Real Estate, managing a substantial $10 billion mortgage portfolio.

The financial institution faced the challenge of extracting critical data from thousands of pages of documents – financial statements, rent rolls, budgets, and projections. With Smart Capital Center, data hidden in multiple pages were processed and transformed into actionable insights within minutes.

Our platform offered real-time, accurate portfolio performance insights, equipping the lender with an accurate snapshot of its portfolio at any moment. Moreover, it provides high-quality, consistent, traceable data, simplified compliance procedures, and increased transparency. This not only led to sizable direct cost savings by reducing manual labor but also revealed significant revenue opportunities.

The result was a testament to the transformative potential of automation, and technology such as Generative AI. The financial institution could automate tasks that take a lot of time. It can also focus on improving property and portfolio insights. Additionally, it can manage risks more proactively and build stronger customer relationships, all while using fewer resources.

As AI improves the work of CRE professionals, it can be both helpful and disruptive in the industry. AI can help workers be more productive. This could lead to economic growth and more jobs.

On the other hand, AI can replace office workers by automating simple tasks. This includes writing legal documents and analyzing financial statements.

A study by McKinsey & Company shows that we can expect a big increase in worker productivity. This will lead to more jobs, higher wages, and overall economic growth.

This growth could help commercial real estate markets. It may create more jobs and lead to economic expansion. This could increase demand for CRE in different property sectors.

However, alongside these optimistic projections, there is also a narrative of potential job displacement due to AI. Historically, every introduction of new technology has sparked fears of widespread job loss. For instance, the rise of robotics in warehouses was anticipated to reduce jobs in that sector. Contrary to these fears, historical patterns show that technological advancements generally result in a net gain of jobs by promoting productivity, though transitional job losses are an inevitable part of the process.

The arrival of the automobile caused a drop in jobs related to horses and buggies. However, it also created many more jobs in car manufacturing and related services. Similarly, despite initial concerns, warehouse jobs have significantly increased in recent years.

The upcoming wave of job displacement may primarily affect white-collar professionals, a shift from the blue-collar seen in recent decades. This could further challenge the office sector, already facing reduced tenant demand due to the rise of remote work. An executive in investment banking highlighted that AI might exacerbate this trend, potentially leading to the obsolescence of certain office roles and affecting demand for non-commoditized office buildings.

Nevertheless, the potential job losses might be counterbalanced by the growing demand for office space from AI firms themselves. While precise employment figures for the AI industry are not definitive, estimates suggest at least 100,000 AI-related jobs currently exist in the U.S.

JLL reports that the AI industry uses more than 17 million square feet of office space. This number could rise to over 60 million square feet in five years if growth continues.

AI is catalyzing employment in adjacent sectors. Salesforce recently announced it will hire 3,300 workers for AI jobs. This comes after previous job cuts. It shows the strong demand in the AI industry.

This changing landscape shows that AI affects commercial real estate in many ways. It could greatly change the sector in the future.

As we move ahead, generative AI technology will bring more advanced uses in CRE lending. We can anticipate the development of more advanced AI models, with enhanced predictive accuracy, refined machine learning algorithms, and an even more seamless integration into various lending processes.

The benefits of LLM technology in CRE lending are becoming increasingly apparent, and as a result, its adoption rates are poised to rise.

A report by Gartner suggests that by the end of 2025, 70% of organizations will have commenced their journey toward integrating AI and ML technology in their operations.

The shift towards embracing GenAI is becoming a critical strategic decision, no longer a question of if but when. Its role in redefining the CRE lending landscape underscores the need for industry players to adapt and evolve, harnessing the power of AI to stay competitive and successful in an ever-changing financial environment.

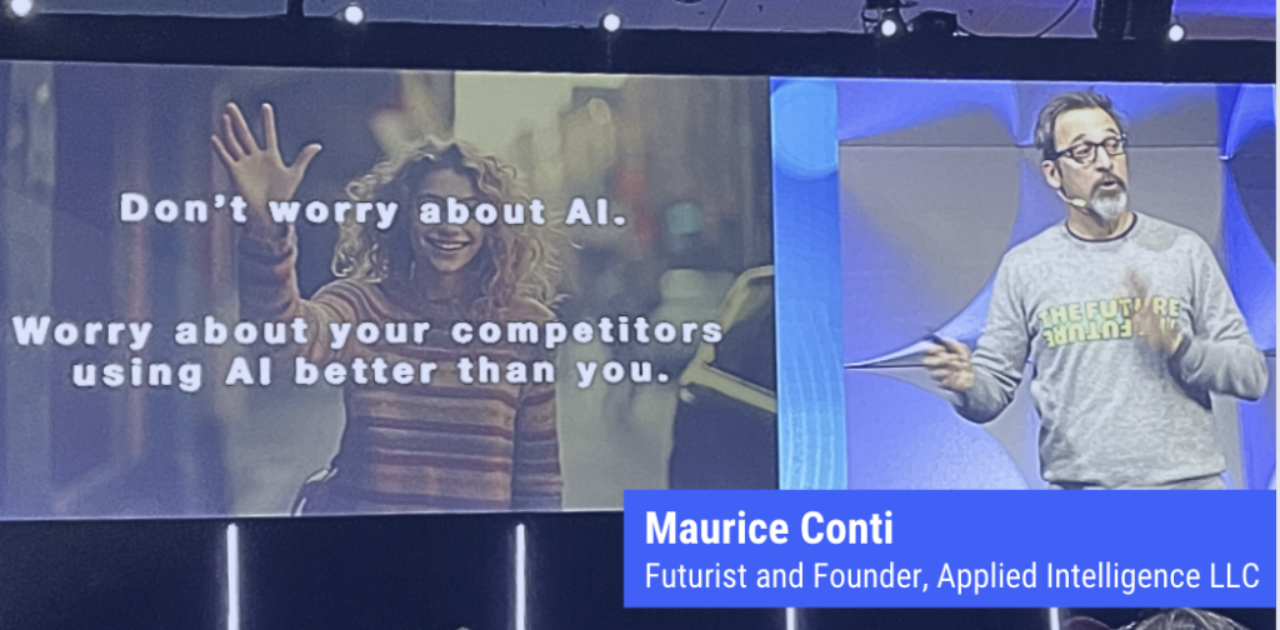

In a presentation made by Maurice Conti at the ULI Fall Conference, he emphasized the transformative impact of AI on the workforce and industry at large. "AI is not going to take jobs," Conti predicted, "It’s going to take tasks." This shift implies that the automation of simpler tasks will liberate workers to engage in more complex and meaningful activities.

Conti's outlook suggests a future where "we will have more jobs rather than less, and they will be higher-value jobs." As automation becomes more prevalent, the bar for employee output is expected to rise. "The expectation will be that you need to do more than you used to, and the only way to do that is with AI."

Another concern often voiced is the fear of superintelligent AI dominating the world. Conti thinks that true artificial general intelligence is at least 50 years away, maybe even 100 years. This gives humanity plenty of time to create plans to reduce any possible threats.

He advises against worrying about the existence of AI itself. Instead, Conti warns, "Worry about your competitor down the street making better use of this technology than you are. That’s the risk." He concludes that companies that effectively leverage AI will emerge as the most resilient in the face of future challenges.

The common problems in the CRE loan process include origination, underwriting, closing, and loan servicing. New digital solutions, such as Smart Capital Center, are addressing these issues.

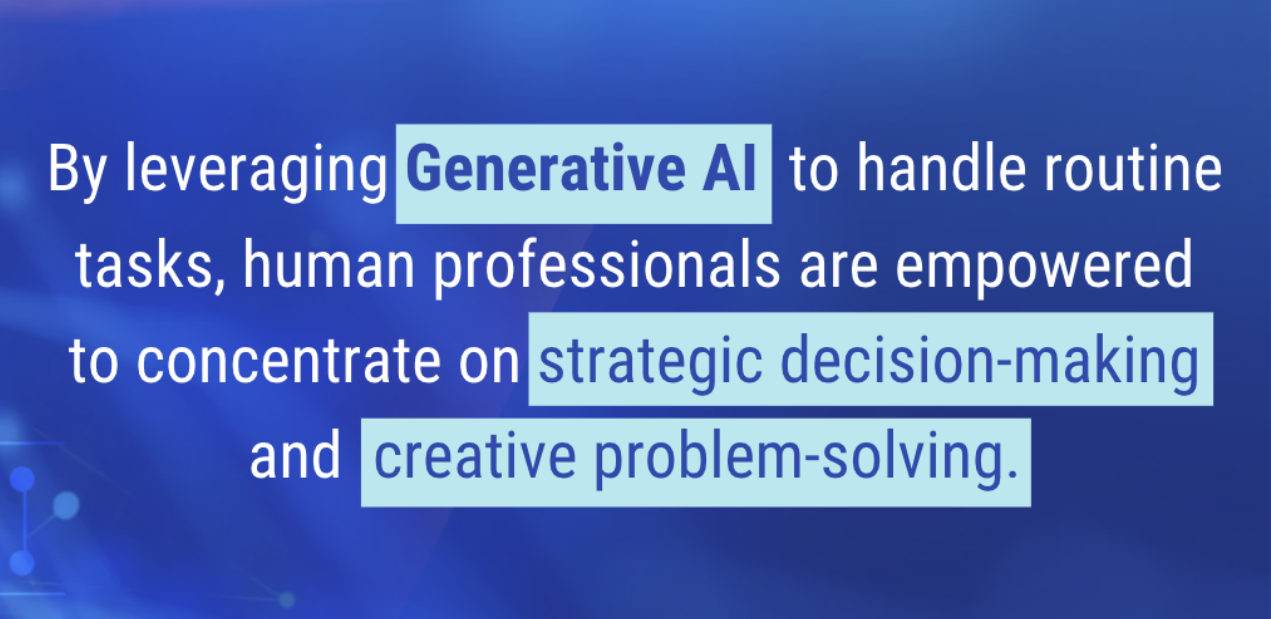

Using Generative AI for routine tasks allows human professionals to focus on important decisions and creative solutions. Innovations like the Smart Capital Center show this change. They highlight a model where human skills and AI work together to enhance both.

Looking to the future, the rapid advancement of LLM technology in CRE lending is undeniable. We are seeing a time when AI and ML algorithms are getting smarter. They are improving accuracy and fitting better into finance processes.

The future of CRE lending will be led by those who use Generative AI technology. They will adapt to its changes and make the most of its potential.

If you want to see how generative AI can help your CRE lending business, keep this in mind. The future is not just something to wait for.

It is something we can build together. Witness this in action by booking a demo with Smart Capital Center today. "Stand at the front of the industry change and help shape the future of CRE finance."

Most lenders see measurable extraction-time savings within the first two weeks of active deployment, primarily on document processing workflows. A Senior Vice President at KeyBank reported a 40% reduction in loan model preparation time mid-implementation, before full platform rollout. Credit memo generation and covenant monitoring improvements typically reach full impact within 60 to 90 days as document volume through the platform accumulates.

Traditional automation handles structured, rule-based tasks: if-then logic, threshold-based alerts, template-driven document assembly. Generative AI handles unstructured inputs — non-standard rent rolls, narrative loan documents, inconsistent borrower submissions — and produces structured, contextually appropriate outputs. The practical distinction: traditional automation requires inputs that already match its templates; generative AI works on the documents lenders actually receive.

Institutional lenders typically combine four controls: private or zero-data-retention enterprise deployments of major LLMs, SOC 2 Type II-compliant infrastructure, data anonymization layers that strip identifying information before LLM exposure, and contractual guarantees that submitted data is never used for model training. Smart Capital Center implements all four, with SOC 2 Type II compliance, AES-256 encryption in transit and at rest, U.S.-based private servers, and contractual exclusion from any model training.

The relevant test is whether the AI platform maintains a source-level audit trail — every figure in the credit memo traceable to the specific document line that produced it. Platforms that meet this standard generate credit packages that satisfy both internal committee review and examiner provenance requirements. According to recent OCC and FDIC examination cycles, the documentation standard for benchmark assumptions and underwriting inputs has tightened, making source traceability a regulatory imperative as well as an internal credit standard.

The effect is bidirectional. AI-driven productivity may reduce demand for certain professional office roles, accelerating office demand softness already driven by remote work. Simultaneously, the AI industry is a major office occupier — JLL research indicates more than 17 million square feet currently occupied by AI firms, with projections of 60+ million square feet within five years. Net effects vary materially by market: AI-concentrated metros (San Francisco, New York, Austin, Seattle) see direct demand support; markets without AI sector presence face the productivity displacement without the offsetting demand growth.

According to Gartner research, the majority of large enterprises are projected to have operationalized generative AI in at least one core business function by 2026, with financial services among the leading adoption sectors. For CRE lending specifically, deeper integration — generative AI as infrastructure rather than tool — is likely a 24- to 36-month process for most institutions, depending on the complexity of existing systems and the depth of regulatory review required for deployment.

The competitive case for adoption is strongest for mid-size lenders. Large institutions have the resources to build internal AI capabilities; small institutions can defer adoption with less competitive consequence. Mid-size lenders face the tightest competitive pressure: they compete against large institutions with scale advantages and against small institutions with relationship advantages. Operationalizing AI is the most accessible way for mid-size lenders to differentiate on execution velocity and analytical depth without expanding headcount.

.png)