AI in Commercial Real Estate

July 13, 2026

AI in Commercial Real Estate

July 13, 2026

Image Source: ChatGPT generated image showing Generative AI in Commercial Real Estate

Generative AI is no longer experimental in commercial real estate lending. According to a Celent / Zest AI survey of 106 U.S. lenders, 67% have completed or will implement GenAI strategies by 2026, and 83% are increasing their GenAI budgets. Institutions deploying purpose-built AI underwriting platforms are reporting 40–60% reductions in analyst time per commercial loan and 50–75% reductions in time-to-decision. With the Mortgage Bankers Association projecting $806 billion in 2026 commercial mortgage originations, capturing share now depends on speed — and speed is where generative AI has its largest measurable impact.

The commercial real estate (CRE) industry is being reshaped by three forces at once: a $1.5+ trillion refinancing wave, structural shifts in lender mix, and the rapid maturation of generative AI. Smart Capital Center sits at the intersection of all three, with an AI-powered platform used by KeyBank, JLL, RGA, Pacific Life, and The RMR Group for underwriting, portfolio insight, and debt management.

This two-part series breaks down where generative AI is genuinely changing CRE lending — and where the limits still are. Part 1 covers the foundational shifts:

Part 2 picks up with credit memo workflows, communications, and legal review.

The story in one line: Generative AI is the subset of AI that creates new content, analysis, or code from learned patterns — not just classifies or predicts existing data. That distinction is the reason it changes CRE lending workflows where prior AI didn't.

Generative AI is a class of artificial intelligence that produces new content — text, images, code, structured data — based on patterns learned from training data, rather than only classifying or scoring existing data.

The current frontier is set by a small number of large language model (LLM) families:

The choice of model matters less than the discipline of the workflow built around it. Most CRE deployments now use multi-model architectures, routing different tasks to different models based on cost, latency, and accuracy.

Purpose: Traditional AI is designed mainly for analysis, interpretation, and decision-making based on existing data. Generative AI, on the other hand, focuses on creating new data and content.

Data Handling: While traditional AI models might classify, sort, or respond to data, generative AI models use their training to produce entirely new data that are similar to but separate from the training data.

Complexity and Computational Power: Generally, generative AI models are more complex and require greater computational power than traditional AI models. This is because they need to understand and replicate patterns in data to generate new, coherent outputs.

Generative AI represents a significant leap in the capabilities of artificial intelligence, moving from understanding the world as it is to imagining and creating things that never existed before.

The story in one line: Most early CRE deployments of generative AI handled administrative tasks; the 2026 deployments are now sitting inside underwriting, credit decisions, and portfolio surveillance — and the productivity numbers reflect that shift.

The first wave of generative AI in CRE concentrated on low-stakes administrative work — scheduling tours, drafting marketing copy, basic customer service. By 2026, the picture has changed materially.

According to the Celent / Zest AI 2025–2026 Generative AI in Lending Survey of 106 U.S. banks, credit unions, and consumer finance companies:

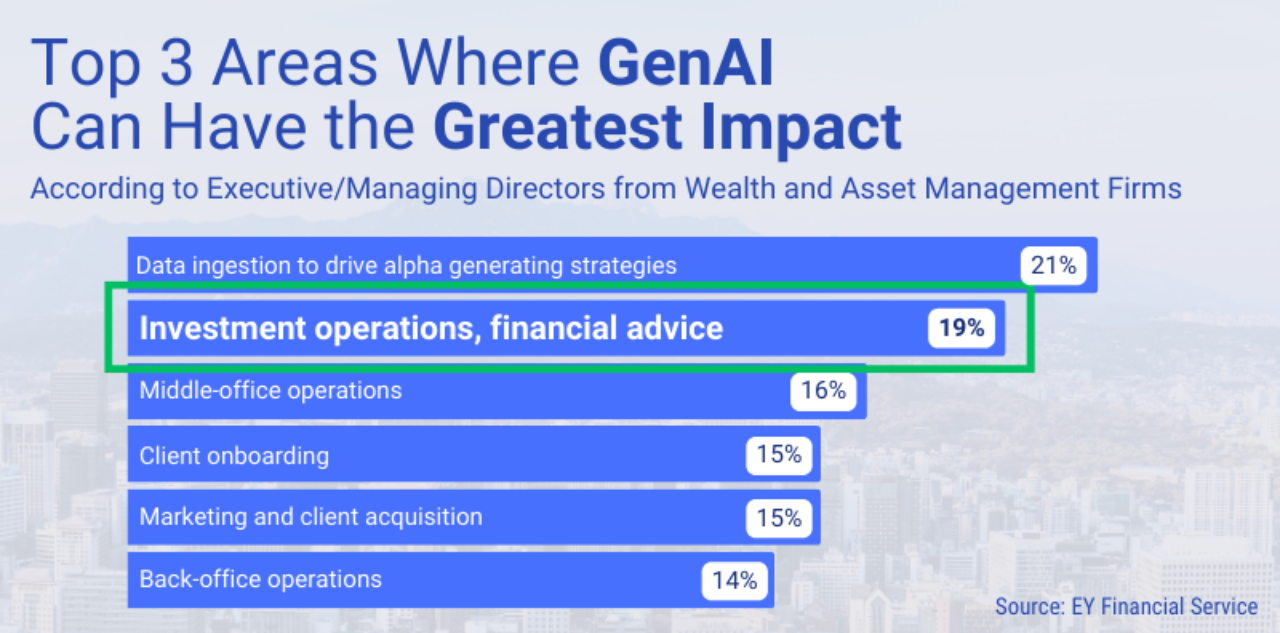

Within CRE specifically, the adoption pattern has narrowed to four high-ROI use cases:

That said, real adoption pain exists. According to McKinsey's late-2025 State of AI survey, nearly nine of ten companies have deployed AI in at least one function — but 94% report not yet seeing "significant" value from those investments. The institutions converting AI into measurable performance are the ones treating it as a workflow redesign rather than a chatbot bolted onto an existing process.

The story in one line: McKinsey estimates generative AI will add $2.6–$4.4 trillion annually to the global economy, with $200–$340 billion of that landing in banking alone — and CRE lending is one of the most concentrated extraction points within banking.

Generative AI is now a systems-level technology, not a single-tool productivity boost. According to McKinsey's analysis of 63 generative AI use cases across 16 business functions, the technology could add the equivalent of $2.6 trillion to $4.4 trillion annually to the global economy, with banking capturing $200–$340 billion of that value.

Three structural impacts are now visible in financial services:

"Just as electricity transformed almost everything 100 years ago, today I actually have a hard time thinking of an industry that I don't think AI will transform in the next several years." — Dr. Andrew Ng, AI researcher and founder of DeepLearning.AI

Critically, generative AI is changing the nature of work, not eliminating it. The model now consistently used by leading institutional CRE platforms is human-in-the-loop: AI handles ingestion, structuring, and first-draft generation, and analysts review, verify, and add judgment.

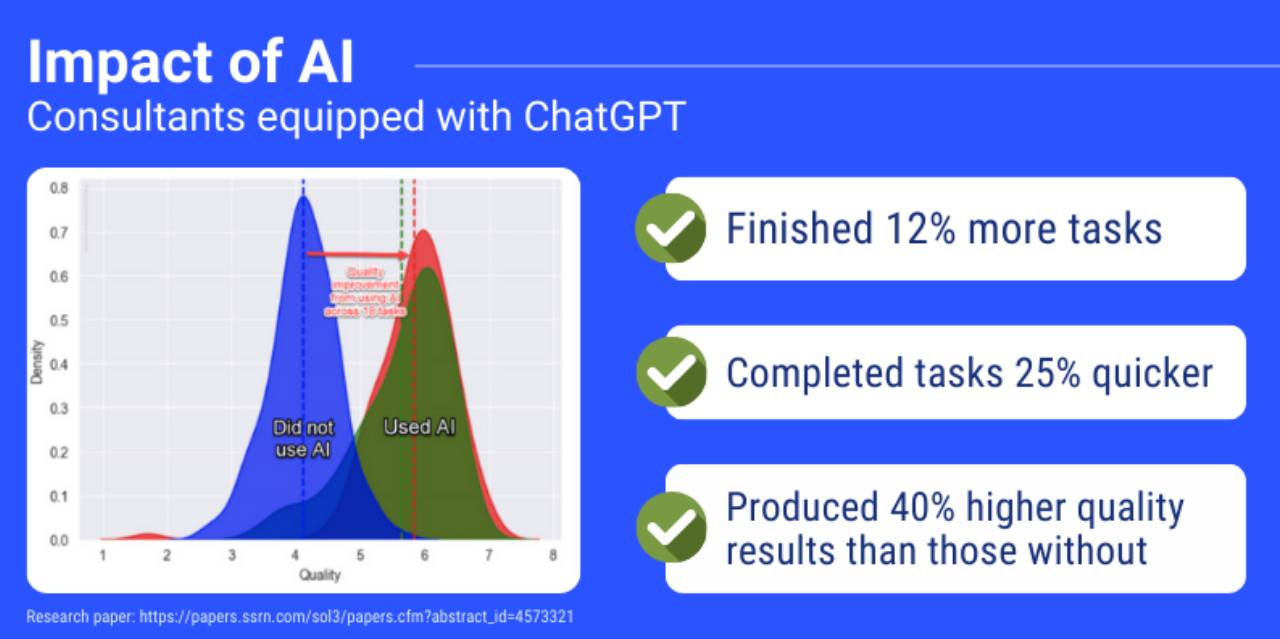

The story in one line: Controlled studies now consistently show 20–70% productivity gains and meaningful quality improvements for knowledge workers using generative AI — and CRE underwriting is the textbook case where both apply.

Early controlled studies have shown sustained time savings of 20–70% across knowledge tasks, paired with measurable improvements in output quality.

The most-cited piece of evidence remains the Harvard / Wharton / MIT / BCG study, which observed 758 Boston Consulting Group consultants performing 18 tasks representative of senior consulting work. The findings:

As artificial intelligence (AI) continues to advance, compelling evidence is emerging about its substantial impact on individual productivity. Early controlled studies have shown remarkable time savings ranging from 20% to 70% across various tasks, coupled with an enhancement in output quality when AI tools are utilized.

A team of social scientists worked with Boston Consulting Group on an experiment. This study showed how AI can change professional settings. This large study looks at the future of professional work in the AI era. It includes 18 tasks that are common in top consulting firms.

The results were striking: consultants utilizing ChatGPT-4 consistently outperformed their counterparts who did not use the AI tool, excelling in every performance metric.

In this study, researchers from Harvard, UPenn, and the University of Michigan looked at consultants using ChatGPT-4. They found that these consultants finished 12% more tasks. They finished tasks 25% faster. Most importantly, the quality of their work was 40% higher than those who did not use ChatGPT-4.

It's important to note that these findings predate the latest enhancements to GPT-4. Recent advancements were not included in the study. These include a new data analytics mode, plugin integration, and updated web search features. This suggests that the productivity gains and quality improvements observed in the study might be even more pronounced with the latest upgrades to GPT-4.

These insights show how AI, especially advanced models like GPT-4, can greatly impact productivity and efficiency at work. As AI keeps evolving, it clearly changes workflows and boosts productivity in many industries. This marks a big shift in how we approach and do work today.

Generative AI is starting to transform the way investment analysis is conducted in the commercial real estate (CRE) sector. Traditional methods had analysts spending many hours analyzing data. Now, AI algorithms can process large amounts of information in just minutes. This technological advancement leads to faster and more accurate analyses, greatly enhancing decision-making efficiency.

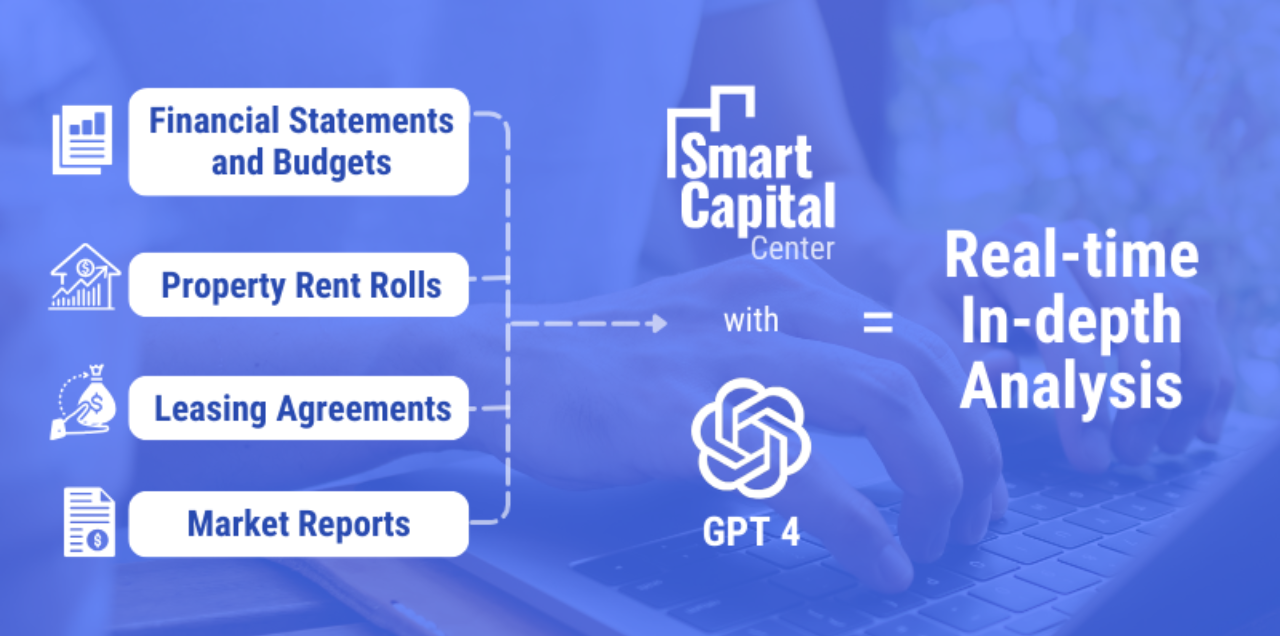

A key player in this transformation is GPT technology, a type of generative AI.

As an AI system, it can collect financial and operating data from loan-related materials. This includes borrower and property financial statements, budgets, rent rolls, leasing agreements, and market reports. This significantly shortens the time needed for data intake, thereby speeding up the entire origination process

The benefits of generative AI extend to the processing of extensive documentation such as information memorandums, market overviews, or due diligence materials. AI shows a promising efficiency in this domain, with the ability to scan, process, and condense large volumes of text into accurate summaries. This capability is particularly valuable in the CRE sector, where the ability to quickly synthesize and analyze complex documents is essential.

This significant reduction in time—from weeks to just a few days—is a testament to the role of GenAI in streamlining the origination process. This initial stage, enhanced by GenAI, lays down a foundation of accuracy and efficiency vital for the subsequent stages of the CRE loan cycle.

Generative AI has real limits that any institutional deployment must address.

Limit 1: Generative AI primarily processes structured or text-based input. A scanned PDF financial statement cannot be analyzed directly by a base LLM. The work-around is a preprocessing layer that converts unstructured documents into structured datasets. Smart Capital Center's platform performs this layer — taking scanned financial statements, rent rolls, Excel spreadsheets, text entries, and complex financial reports and converting them into a uniform dataset ready for downstream AI analysis.

Limit 2: Output accuracy must be reviewed by humans. Generative AI is fluent but not infallible. In CRE underwriting, where precision is non-negotiable, every AI output must be verified by an analyst. As a Keyway / Appraisal Institute survey of ~200 CRE firms found in late 2025, investment committees still distrust AI-generated analysis they cannot trace to source data.

A concrete example: when generating a unit mix and excluding vacant units, a model may misinterpret a subtotal row as a separate unit type. In Advanced Data Analytics mode, the model can flag the row as a likely subtotal — but a human still needs to confirm. Explicit prompts ("ignore subtotal rows") materially improve accuracy.

Limit 3: Model outputs need to be paired with source-traceable provenance. Audit-ready CRE workflows require that every number in a credit memo or underwriting model can be traced back to the source document. Smart Capital Center's platform retains that provenance natively, which is what makes it appropriate for institutional use cases — KeyBank, JLL, RGA, Pacific Life, The RMR Group — where examiners and credit committees need to see the trail.

The combination of generative AI fluency and human verification is what produces institutional-grade analysis. Either one alone is insufficient.

The story in one line: AI underwriting is now compressing analyst time per commercial loan by 40–60% and time-to-decision by 50–75% — and the lenders capturing those gains are competing for share in a $806 billion 2026 origination market.

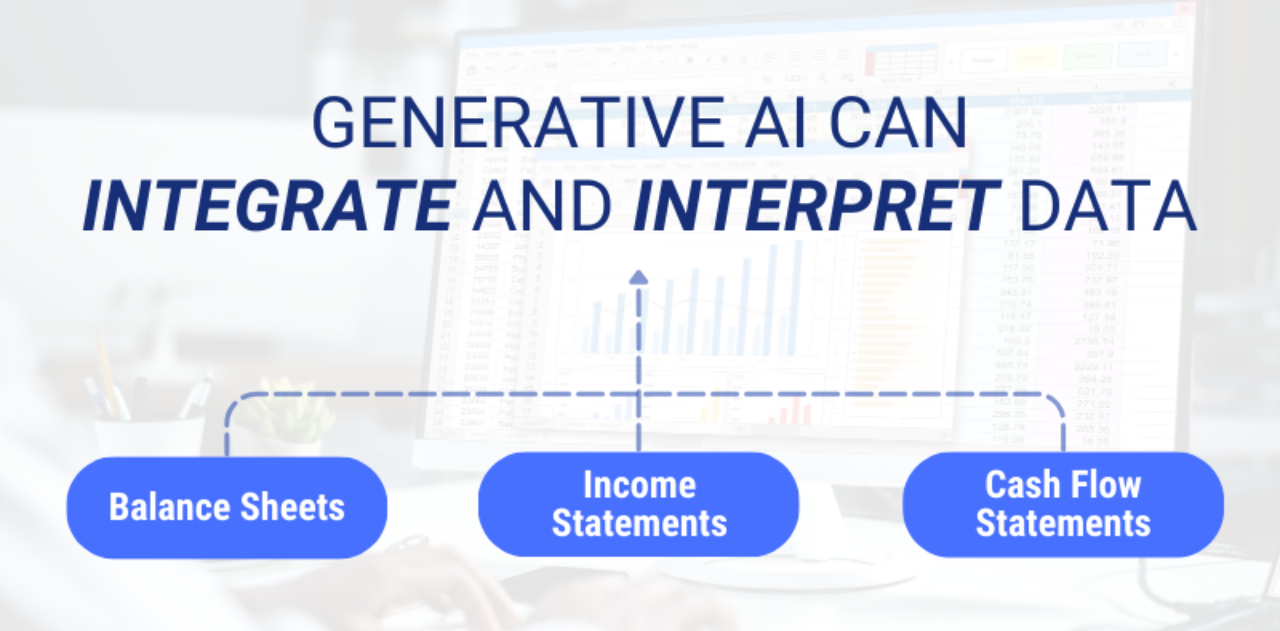

Generative AI is changing every step of the underwriting process for lenders and asset managers. Modern systems synthesize large volumes of financial data, interpret complex patterns, and project forward financial health — the core inputs for every lending decision.

AI can integrate financial statements, balance sheets, rent rolls, development budgets, and operating projections to assess borrower stability and property profitability. Advanced algorithms evaluate historical financial performance, project cash flows, and surface risks and opportunities that manual review can miss.

Automated systems using generative AI also model debt service capacity using real-time data feeds, keeping underwriting assessments current with property performance and market conditions. Analyses can be reproduced quickly under different rate, occupancy, and cap rate scenarios — replacing what used to be a one-time underwriting exercise with a continuous one.

Smart Capital Center benchmarks underwriting against 1B+ real-time data points across 120M+ properties, has supported $500B+ in CRE transactions, and integrates with Yardi, ARGUS, SS&C Precision, and Midland Enterprise via API.

"Smart Capital Center reduced our financial model prep time by 40%. What used to take three analysts a full day now takes one analyst two hours — with cleaner outputs and full traceability for our loan committee." — Ken Schroeder, KeyBank

For deeper context on how this connects to debt management and portfolio surveillance, see our two-part series on automated CRE underwriting.

The story in one line: AI-driven document review is moving from "supporting tool" to "the actual workflow," with insurance policies, appraisals, leases, and environmental reports reviewed in minutes against pre-defined risk criteria.

Document review and approval — historically one of the most time-intensive bottlenecks in CRE lending — has become a core area of AI deployment. AI can:

With AI, reviewing and approving documents like insurance policies and appraisal reports takes less time.

AI algorithms can quickly scan through documents to identify key terms, conditions, and clauses. This ability lets us quickly check if a document meets the required standards and rules. It greatly cuts down the time needed for manual review.

AI systems can find potential risks and problems in documents. They do this by looking for patterns and inconsistencies that humans might miss. This includes finding mistakes in appraisal reports or noticing possible problems in environmental assessments. This ensures that all risks are marked for further review.

AI can automate the workflow. It can send documents to the right people for review and approval.

This is done based on set criteria. This speeds up the process and makes sure all approvals are obtained in the right order. This helps reduce delays.

Beyond just reviewing documents, AI can provide predictive insights based on the content of the documents and historical data. AI can predict how likely an insurance claim will happen. It uses details from the policy and past claims. This helps in making decisions.

What is generative AI in commercial real estate lending?Generative AI in CRE lending refers to large language model-based systems that produce new content, analysis, and structured outputs from heterogeneous loan documents — financial statements, rent rolls, leases, appraisals, and market reports. Unlike traditional rule-based or classification AI, generative AI can draft credit memos, summarize OMs, and generate underwriting analysis from scanned and unstructured inputs.

How much faster is AI-assisted CRE underwriting?Banks deploying AI underwriting have reported 40–60% reductions in analyst time per commercial loan and 50–75% reductions in time-to-decision, according to 2026 industry research. Capturing share in the MBA's projected $806 billion 2026 origination market increasingly depends on this speed differential.

How widely is generative AI adopted in lending today?According to the Celent / Zest AI Generative AI in Lending Survey of 106 U.S. lenders, 67% have completed or will implement GenAI strategies by 2026, and 83% are increasing their GenAI IT budgets, with 41% expecting increases above 5%. GenAI is now adopting faster than every prior lending technology revolution, including AI/ML, online lending, and mobile lending.

What are the limits of generative AI in CRE lending?Three limits matter operationally. First, generative AI processes structured or text inputs natively but cannot directly analyze scanned PDFs without a preprocessing layer. Second, every AI-generated output must be human-verified before it enters a credit memo or committee deck, as a Keyway / Appraisal Institute survey of ~200 CRE firms confirmed that investment committees distrust AI-generated analysis without source-data traceability. Third, regulatory frameworks under ECOA, the OCC, FDIC, and CFPB require that AI-driven credit decisions remain explainable.

Which large language models are used in CRE lending?Most production CRE deployments use a mix of GPT-class models from OpenAI, Claude models from Anthropic, Gemini from Google, and open-weight Llama models from Meta. The choice is workflow-driven: long-context document analysis often runs through Claude, while broader chat-based tasks run through GPT or Gemini. Multi-model architectures are now common, with task routing based on accuracy, latency, and cost requirements.

How much economic value will generative AI create in banking?McKinsey estimates generative AI will add $2.6–$4.4 trillion annually to the global economy across 63 use cases, with $200–$340 billion of that landing in the banking sector specifically. McKinsey notes, however, that 94% of companies that have deployed AI report not yet seeing significant value — the value is concentrated among institutions treating AI as a workflow redesign rather than as a chatbot bolted onto an existing process.

How does Smart Capital Center use generative AI in underwriting?Smart Capital Center's platform converts unstructured loan documents — scanned financial statements, rent rolls, leases, market reports — into a standardized dataset, then applies AI underwriting against 1B+ real-time data points across 120M+ properties. Outputs are source-traceable for credit committee and audit review. The platform has supported $500B+ in CRE transactions and is used by KeyBank, JLL, RGA, Pacific Life, and The RMR Group. Book a demo to see it applied to your portfolio.

To discover further applications of generative AI in CRE, head to Part 2 of this article.

.png)