CRE Asset Management

June 16, 2026

CRE Asset Management

June 16, 2026

The 2026 multifamily financing environment has split in two directions at once. On one side, the MBA reports $875 billion of CRE mortgages maturing in 2026 — including a 56% jump in multifamily-specific maturities to $162.1 billion (MMG Real Estate Advisors). On the other, lending capacity is at a multi-year high: the MBA forecasts $805 billion in 2026 CRE originations, debt funds and mortgage REITs led 37% of non-agency closings in 2025, and Fannie Mae and Freddie Mac's combined multifamily cap rose 20% to $176 billion. The borrowers who succeed in 2026 are the ones who treat alternative capital, agency execution, and AI-driven debt management as a single playbook — not three separate options.

The traditional bank-driven multifamily financing playbook has been rewritten over the last 24 months. Borrowers refinancing today are facing a different rate environment, a different lender mix, and a different underwriting standard than the one that originated their existing loans. Smart Capital Center helps multifamily investors and lenders navigate that shift with AI-powered underwriting, lender matching across 1,000+ capital sources, and proactive debt management — so capital decisions are made on real-time market data rather than on relationships and spreadsheets.

This article covers four things you need to navigate 2026:

The story in one line: The Fed has begun cutting rates and lending capacity is at a multi-year high — but multifamily borrowers refinancing into 2026 still face rates roughly double what they originated at, and the maturity wall is now arriving in earnest.

After the historic 2022–2023 hiking cycle, the Fed delivered 25 basis-point cuts in September and October 2025 (MMG Real Estate Advisors, 2026). Borrowing costs have come off their peaks, but they remain materially above the 3%–4% rates at which most current multifamily loans were originated.

That gap is the core of the refinancing problem.

According to the Mortgage Bankers Association's 2025 Commercial Real Estate Survey of Loan Maturity Volumes, 17% — or $875 billion — of the $5 trillion in outstanding CRE mortgages will mature in 2026. While that's a 9% decline from 2025's $957 billion, it's still nearly triple the 20-year average.

"While commercial mortgage maturities remain elevated in 2026, the 9% decline from 2025 suggests that the market is beginning to move past the peak of the maturity wave in recent years." — Reggie Booker, Associate Vice President of Commercial Research, Mortgage Bankers Association

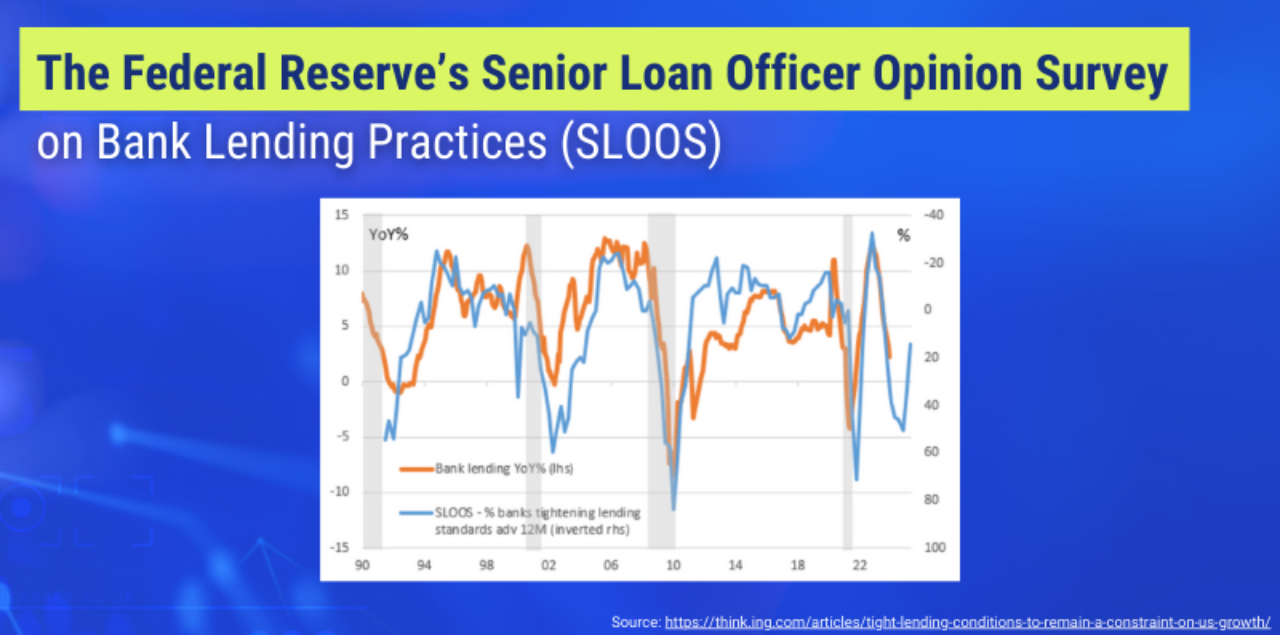

Source: Think ING - Tight Lending Conditions to Remain a Constraint on US Growth

The picture from the January 2026 Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) is meaningfully different from the 2023 narrative:

Takeaway for borrowers: The lender posture in 2026 is "selectively open," not "broadly closed." Banks are willing to do deals — but they are doing them on tighter LTVs, conservative debt yields, and sponsor strength they can verify quickly. Borrowers who can present clean, automated underwriting packages are converting; those still relying on manual diligence are losing weeks at exactly the moment when speed matters most.

The story in one line: Alternative capital is no longer "alternative" — debt funds and mortgage REITs led 37% of non-agency multifamily closings in 2025, and 63% of submitted deals in Q4 2025 went to private lenders first (LoanBase, Feb 2026).

As traditional bank financing remains selective, multifamily investors must build a capital stack from a wider pool of sources than ever before. Alternative financing is no longer a fallback — it is now where the majority of CRE deal flow is being processed.

In multifamily investments, creative capital solutions are any financing structures that fall outside standard 5- to 10-year bank loans or agency mortgages. They include private debt funds, mortgage REITs, mezzanine and preferred equity, agency execution at higher LTVs, tax credit financing (LIHTC, HTC), property-assessed clean energy (PACE) financing, master leases, and CRE collateralized loan obligations (CRE CLOs).

These structures share one trait: they exist because the standard bank loan no longer covers the gap between rising acquisition prices and conservative LTVs.

The world of real estate finance is undergoing a notable transformation. Long-dominant traditional banks, known for their straightforward lending structures, are losing some of their market share. In their place, Wall Street-powered debt funds are emerging as key players, bringing along several key changes:

Our AI-powered platform connects investors with an expansive network of over 1,000 lenders. This technology-driven approach ensures that investors receive bank-quality property underwriting, cutting financing costs and free, real-time loan quotes with a same-day response. This smooth process removes the long wait times usually linked to loan applications. It makes sure you get the best terms available.

The most common error is becoming fixated on which lender funds the deal rather than on whether the deal pencils on the terms offered. With private lender pricing 2–4% above bank rates (Northwind Group) and CRE CLO floating-rate exposure now at its highest share of new originations since 2021 (Trepp / CRE Daily, 2026), the debt structure can swing total returns by 200–400 basis points before any operating performance is considered.

Successful borrowers stress-test cash flow under three scenarios before committing:

If the deal still generates positive levered cash flow under all three, the financing source is workable. If not, the financing is masking a deal problem.

In 2026, capital is broadly available — but the difference between the best execution and the second-best is meaningful. Brokers and platforms are now routing the same deal to 5–8 lenders before recommending one, and pricing dispersion across capital sources for the same multifamily asset can run 75–150 basis points in spread.

The opportunity cost of accepting the first quote is real. Borrowers should solicit competing terms across at least three capital sources (typically: agency, bank, and debt fund) before committing.

Exploring different financing strategies is important in today's multifamily investment world. It is also vital to use these methods wisely and sustainably. Here are two key secrets to successful alternative financing:

By utilizing an AI-powered platform, investors gain a 360-degree view of their debt. This real-time visibility and proactive analysis empower them to make informed decisions about their financing strategies, maximizing returns, and minimizing risk.

Multifamily investors can manage the challenges of alternative financing. They can do this by focusing on sustainable money flow. They should also find good financing options and use AI. They can do this while keeping a disciplined and strategic approach.

This mindset boosts the chances of success. It also helps create long-term growth and stability in multifamily investments.

The multifamily financing landscape is evolving rapidly, and property investors must be willing to adapt and compromise to secure viable investment opportunities. As traditional bank financing becomes increasingly challenging, embracing alternative strategies is no longer just an option but a necessity.

In an article released by The Economics Time about ‘Entrepreneurship and Adaptability’, it says, “By staying open to new ideas and approaches, entrepreneurs can capitalize on market disruptions and create innovative solutions that meet evolving customer needs. Successful entrepreneurs understand that the ability to adapt is crucial for staying relevant and staying ahead of the competition.”

As we accept that higher rates are here to stay, operators must learn to work in this new financing environment. This means taking a proactive approach to managing debt. Stay informed about market changes and be ready to adjust your strategies. Alternative financing strategies are becoming more popular. Experts believe that the multifamily financing landscape will keep changing. This means investors need to stay flexible and informed.

The market will likely see more consolidation in lending. Specialized lenders and alternative financing platforms will play a bigger role. investors who can leverage technology and strong industry partnerships will be well-positioned to navigate the evolving market dynamic.

Smart Capital Center helps property investors navigate the complexities of the multifamily financing market. Smart Capital Center has a wide network of lenders. They use advanced AI for underwriting. They are dedicated to offering the best terms. This makes them a great choice for multifamily investors looking for alternative financing solutions.

How much CRE debt is maturing in 2026?

According to the Mortgage Bankers Association's 2025 Commercial Real Estate Survey of Loan Maturity Volumes, $875 billion — or 17% of the $5 trillion in outstanding CRE mortgages — will mature in 2026, a 9% decrease from 2025's $957 billion peak. Multifamily-specific maturities jump 56% from $104.1 billion in 2025 to $162.1 billion in 2026 (MMG Real Estate Advisors).

Are multifamily lending standards getting easier in 2026?

Yes — modestly. The January 2026 Federal Reserve SLOOS reported that a modest net share of banks eased standards on multifamily loans in Q4 2025 — the first net easing in more than two years. Large banks led; smaller community banks remained more cautious. Banks expect overall CRE credit quality to improve in 2026.

What share of multifamily lending is now done outside of banks?

According to CBRE data published in early 2026, debt funds and mortgage REITs led non-agency closings with approximately 37% of volume in 2025, followed by banks at 31% and life insurance companies at 16% — a sharp shift from 43% life-company share in 2024. Brokers reported that 63% of submitted deals in Q4 2025 routed to private lenders first (LoanBase).

How much higher are debt fund rates compared to bank rates?

According to Ran Eliasaf, Founder and Managing Partner of Northwind Group, private lenders typically charge interest rates 2% to 4% higher than bank loans, in exchange for higher LTV ratios and faster execution. The trade-off is real: debt fund execution can close in weeks versus months for bank loans, but the all-in cost of capital is materially higher.

What is creative capital in multifamily real estate?

Creative capital refers to any multifamily financing structure outside standard bank loans or agency mortgages. The most common 2026 instruments include private debt funds, mortgage REITs, CRE CLOs (which made up 70% multifamily collateral in early 2026), LIHTC and Historic Rehabilitation Tax Credits, PACE financing for energy retrofits, master lease structures, and mezzanine/preferred equity.

How are agency multifamily caps changing in 2026?

The Federal Housing Finance Agency raised the combined Fannie Mae and Freddie Mac multifamily loan purchase caps for 2026 to $176 billion — roughly a 20% increase over 2025 capacity (CRE Daily, 2026). Agency execution is now anchoring stabilized multifamily refinance rates near 5%.

How does Smart Capital Center help multifamily investors find the right financing?

Smart Capital Center's AI-powered platform connects investors with a network of more than 1,000 lenders, delivers bank-quality property underwriting, and surfaces real-time loan quotes with same-day response. The platform analyzes 1B+ real-time data points across 120M+ properties, has supported $500B+ in CRE transactions, and is used by KeyBank, JLL, RGA, Pacific Life, The RMR Group, and other institutional investors and lenders. Book a demo to apply it to your next deal.

What should multifamily investors prioritize when choosing a financing structure?

Three priorities: (1) test cash flow under base, downside, and refinance scenarios before signing — debt structure can swing levered returns by 200–400 bps; (2) solicit competing quotes across at least three capital sources (typically agency, bank, and debt fund) given pricing dispersion of 75–150 bps for the same asset; (3) put proactive debt management in place to monitor covenants, key dates, and refinance windows continuously rather than reactively.

.png)