July 16, 2026

According to the Mortgage Bankers Association's 2025 CRE Survey of Loan Maturity Volumes (March 2026), $875 billion — 17% of the $5 trillion in outstanding U.S. commercial mortgages — will mature in 2026, and S&P Global Market Intelligence projects the wall will keep climbing toward $1.26 trillion in 2027 (MBA, March 2026; S&P Global / CRE Daily, October 2025).

The MBA CREF 24 conference in San Diego, held two years before that data landed, set the table for exactly this environment. As a cornerstone event for the commercial and multifamily finance industry, MBA CREF 24 brought top professionals together to discuss the trends, regulatory shifts, and innovative strategies that have since defined the cycle. This article uses Smart Capital Center — the AI-powered CRE intelligence platform analyzing 1B+ real-time data points across 120M+ properties and $500B+ in transactions for clients including KeyBank, JLL, and the Community Preservation Corporation — as the lens for that recap.

Below are the trends and takeaways from MBA CREF 24 covered in this article:

• Driving Affordability and Safety in Housing: Prioritizing Workforce Initiatives and Tenant Protections

• $929 Billion in Commercial Mortgages Nearing Maturity

• CPI Surge Driven by Shelter Costs Signals Shift in Real Estate Market Dynamics

• Investment Expectations Shift with Rising Inflation and the Repercussions for Real Estate Financing

• Transforming Mortgage Transactions in a Volatile Market with AI-Powered Solutions

Driving Affordability and Safety in Housing

MBA CREF 24 surfaced several issues that continue to shape lender behavior in 2026: workforce housing, tenant protections, and the challenges around property conditions and insurance. The Joint Center for Housing Studies of Harvard University reported in 2025 that the U.S. is short roughly 1.5 million units of affordable rental housing for households earning under 80% of area median income — the gap MBA CREF 24's affordability discussion was designed to address.

Kevin Palmer, Senior Vice President and Head of Multifamily at Freddie Mac, emphasized the significance of workforce housing at the conference, framing the Workforce Housing Preservation Program as a liquidity-and-credit lever: "This is where sponsors agreed to set aside a certain portion of their units, and keep them affordable for a period of time…basically for the whole duration of that loan. And by doing so we kind of lean in from a pricing and credit perspective, and it really helps to support the liquidity in that important space."

Michele Evans, Executive Vice President and Head of Multifamily at Fannie Mae Multifamily, introduced the Sponsor-Dedicated Workforce product the same year — a structure that simplifies industry compliance by focusing on rent restrictions over income limitations. By 2025, Fannie Mae and Freddie Mac together backed a record share of multifamily originations, in part on the back of these workforce housing structures (Federal Housing Finance Agency, 2025).

Tenant protections were a parallel theme. Palmer underscored the value of "good decent safe housing, that families can be proud of and that helps to advance them individually and economically," pointing to community-building efforts and the need for further data collection on tenant notification protections. Freddie Mac's 2023 borrower feedback prompted explicit policy adjustments aimed at improving property safety and condition surveillance — adjustments that have carried into post-2024 underwriting requirements.

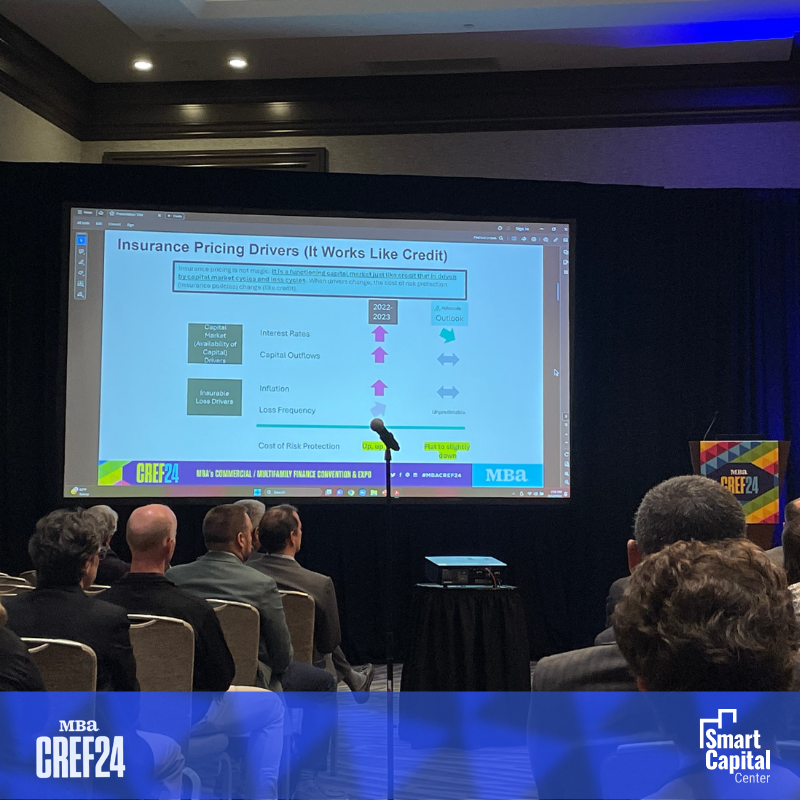

On property insurance, Evans framed the dialogue collaboratively: "Whenever you see challenges like this, I think there's a great opportunity for the entire industry to get together, and really kind of take a look at it and see what we have, and what we can do, and how we can think about it." By 2025, CBRE reported insurance had become one of the top three cost-pressure items in multifamily underwriting, particularly in coastal and wildfire-exposed markets.

PRACTICAL TAKEAWAY

Workforce housing programs and insurance review are no longer side topics — they sit alongside DSCR and LTV in any sponsor-led multifamily refinance review. Run insurance adequacy as a standalone underwriting workstream, not a closing-week formality.

$929 Billion in Commercial Mortgages Nearing Maturity

MBA CREF 24 broke the news that 20% of the $4.7 trillion in outstanding commercial mortgages — $929 billion — was scheduled to mature in 2024, a 28% increase from the $729 billion that matured in 2023. Two years later, the maturity wave has not subsided. According to the MBA's 2025 CRE Survey of Loan Maturity Volumes, $875 billion — 17% of the $5 trillion now outstanding — will mature in 2026, and S&P Global Market Intelligence projects the wall will peak at $1.26 trillion in 2027.

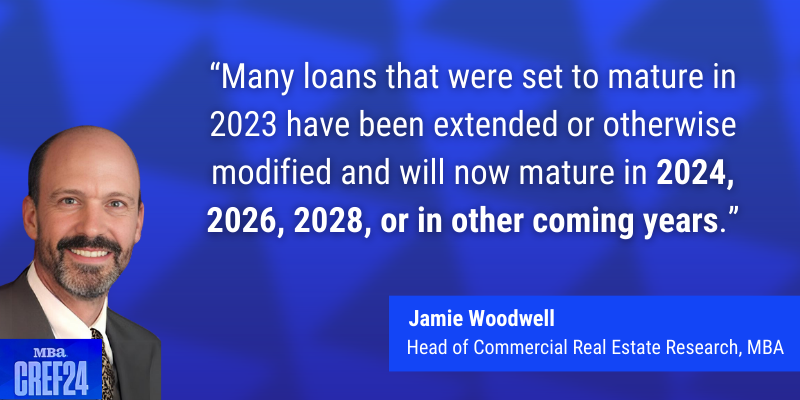

Jamie Woodwell, Head of Commercial Real Estate Research at MBA, attributed the 2024 spike to suppressed transaction activity in 2023 and to lender flexibility on extensions and modifications: "The lack of transaction and other activity last year, coupled with built-in extension options and lender and servicer flexibility, has meant that many loans that were set to mature in 2023 have been extended or otherwise modified and will now mature in 2024, 2026, 2028, or in other coming years."

The maturity outlook varies sharply by property type. At MBA CREF 24, the conference shared that 38% of hotel loans, 27% of industrial, 25% of office, 18% of healthcare, 17% of retail, and 12% of multifamily mortgages were set to mature in 2024. Two years on, CBRE's 2026 Outlook reports CMBS office delinquency at 7.29% as of Q2 2025 — the most pressured corner of the market — while multifamily and industrial remain the strongest, with abundant agency liquidity supporting refinance activity.

Woodwell further explained that despite commercial mortgages’ inherent long-term nature, the current landscape is filled with challenges, including market volatility, interest rate uncertainties, and evolving property fundamentals.

Yet, this surge in maturities, combined with uncertainty around interest rates, a lack of clarity on property values, and questions about some property fundamentals have suppressed sales and financing transactions.

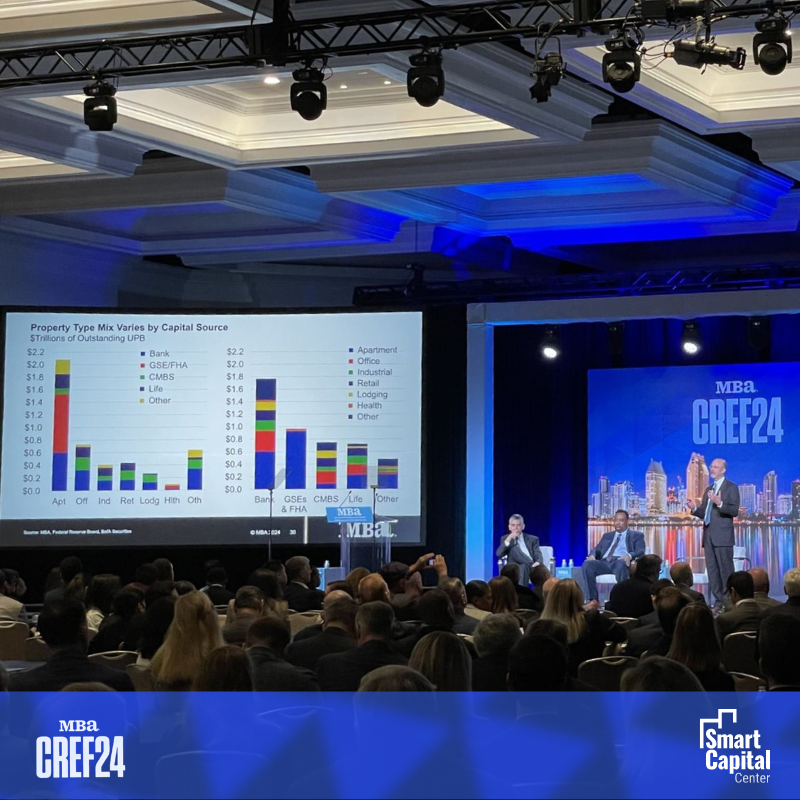

The maturity outlook varies considerably across different segments of the market. Notably, a mere 3% ($28 billion) of the multifamily and healthcare mortgages held or guaranteed by Fannie Mae, Freddie Mac, FHA, and Ginnie Mae are set to mature in 2024.

In contrast, depositories will witness 25% ($441 billion) of their mortgage balances maturing, with CMBS, CLOs, or other ABS seeing 31% ($234 billion), and credit companies, among others, facing a 36% ($168 billion) maturity rate.

The distribution of maturing loans also significantly differs by property type. While 12% of multifamily property mortgages are expected to mature in 2024, the figures rise to 17% for retail, 18% for healthcare, 25% for office properties, 27% for industrial loans, and a stark 38% for hotel/motel loans.

The reported figures represent the outstanding principal balances as of December 31, 2023. It is customary for most loans to reduce their principal over time, so it is expected that the balances upon maturity will be less than the amounts currently stated.

CRE Experts Share Key CRE Trends and Strategies

The closing super session at MBA CREF 24 brought together Maggie Burke (Capital One Commercial Real Estate), Victor Calanog (Manulife Real Estate Finance Group), Kevin Fagan (Moody's Analytics CRE), Adam Fox (Fitch Ratings), and Jan Sternin (Berkadia) for a forward-looking roundup of the cycle ahead.

Their consensus framed three operating priorities for lenders and investors: industry advocacy on regulatory clarity, technology-driven underwriting, and strategic foresight on capital deployment. Two years later, those priorities have aged well. The MBA's February 2026 CREF Forecast projects $805 billion in 2026 originations, a 27% year-over-year increase — a level that requires faster, data-richer underwriting workflows than the 2023–2024 cycle ever required.

CPI Surge Driven by Shelter Costs: Latest Numbers Not as Dire as Market Thinks

It is important to note that the cost of apartment rentals is a significant factor causing shelter inflation to appear much higher than it truly is. This is partly duMBA CREF 24's macroeconomic panels flagged that the cost of apartment rentals was a primary driver of the CPI shelter component appearing higher than underlying market dynamics. The expiration of pandemic-era discounts and concessions was inflating the print. The Bureau of Labor Statistics CPI series subsequently confirmed the framing: shelter accounted for over half of the headline CPI delta in 2024 before moderating through 2025.

That moderation gave the Federal Reserve room to cut its short-term rate target by 100 basis points across 2024 (Federal Reserve Press Releases, 2024–2025), even as long-term yields rose by an equivalent amount. Treating the shelter inflation component as one factor in a broader CPI picture — not the whole story — turned out to be the right call for capital markets pricing.

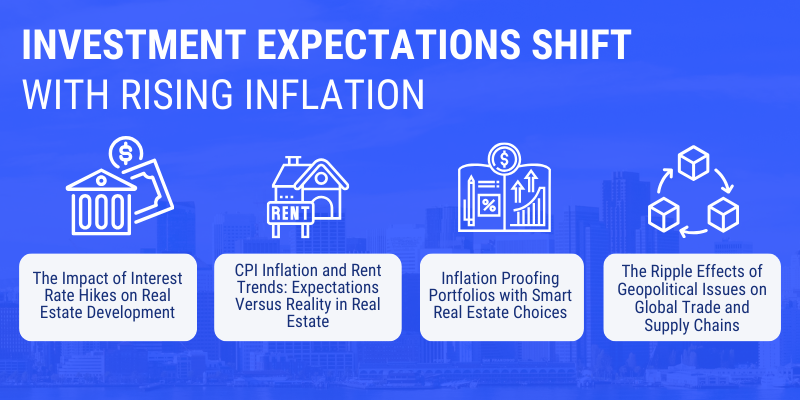

Investment Expectations Shift with Rising Inflation

Inflation reshaped investment expectations across CRE in 2024–2025, in line with what MBA CREF 24 panels predicted. The Fed's preferred inflation gauge — core PCE — is now within 0.4 percentage points of the 2% target (Federal Reserve, 2025), which means the conversation has shifted from "will inflation crush deals" to "how do we underwrite under sticky-but-falling inflation."

The Impact of Interest Rate Hikes on Real Estate Development

Panelists at MBA CREF 24 framed it directly: "The surge in rates is making numerous deals challenging to justify, particularly those involving value-add strategies in equity investment scenarios." Two years on, that thesis is largely intact. CBRE's 2026 Outlook expects long-term yields to stabilize near 4%, with cap rate compression of 5 to 15 bps for most property types — a tailwind for refinance LTVs but a continued headwind for value-add deal economics.

Another panelist captured the operating reality: "Critical decisions often hinge on forecasting where the 10-year Treasury will land, influencing whether we proceed or decline substantial investment opportunities, particularly when the math on building costs doesn't add up." Borrowers responded by pivoting to shorter-duration loans — a behavior the MBA expects to continue into 2026.

CPI Inflation and Rent Trends: Expectations Versus Reality in Real Estate

MBA CREF 24 highlighted the historical lag between asking rents and CPI shelter inflation, predicting an eventual alignment. The Yardi Matrix multifamily series shows asking rents grew 1.2% in 2024 — well below CPI shelter — and have re-converged with the CPI print through 2025. The Fed's expectation that overall inflation gradually returns to its 2% target has held up.

This realignment matters for every loan committee currently underwriting a refinance: rent growth assumptions baked into 2022–2023 underwriting are no longer conservative. Refresh asking-rent comps against current submarket data — not a 24-month-old appraisal.

Inflation Proofing Portfolios with Smart Real Estate Choices

Real estate is widely cited as an inflation hedge, but the 2024–2025 cycle confirmed the hedge is asset- and structure-specific. According to the NCREIF Property Index, industrial and multifamily delivered the strongest inflation-adjusted returns through the cycle, while office underperformed by a wide margin.

The strategic implication: portfolio composition matters more than "real estate exposure" as a category. Run inflation-adjusted return scenarios per property type, not at the aggregate level, when rebalancing capital allocation.

The Ripple Effects of Geopolitical Issues on Global Trade and Supply Chains

MBA CREF 24 flagged geopolitical disruption as the dominant risk to the supply side of the inflation equation, with shipping costs up over 100% in some lanes during the prior six months. The Drewry World Container Index later confirmed the spike, with composite container rates peaking in mid-2024 before easing through 2025.

"The supply side of the equation has changed," one panelist noted. That observation aged well — and the operational lesson for CRE is that any project sensitive to construction inputs or imported materials should price geopolitical disruption as a named risk in the underwriting model, not as a contingency.

Experts Predict a Near-term Decrease in Interest Rates

MBA CREF 24's panelists were broadly aligned on near-term rate cuts. They got the direction right. The Federal Reserve cut its short-term rate target by 100 basis points in 2024 (Federal Reserve, 2024), and most 2026 forecasters expect one to two additional cuts before year-end.

The more important nuance: long-term yields rose by an equivalent 100 bps over the same window. The yield curve is now steeper than at any point during MBA CREF 24, and borrowers are pivoting to shorter-duration loans rather than waiting for long rates to fall. The MBA expects $805B in 2026 originations on the back of this dynamic — a 27% year-over-year increase.

Federal Reserve Targets Employment and Price Stability for Economic Health

MBA CREF 24 panelists framed the Fed's dual mandate clearly: full employment and price stability, monitored via the unemployment rate and the Personal Consumption Expenditures (PCE) index. Their working threshold — a PCE print at or below 2.5%, paired with unemployment moving toward the 4–5% range, would justify rate cuts — has held up against the data.

As of late 2025, the U.S. unemployment rate sits at 4.2% and core PCE at 2.4% (U.S. Bureau of Labor Statistics, 2025; Federal Reserve, 2025) — both inside the bands the MBA CREF 24 panel flagged as the trigger for additional Fed action. The panel's read on what the Fed was watching, and why, was substantively correct.

Rising Construction Costs Add Complexity to Real Estate Development

A construction cost expert at MBA CREF 24 made a single, durable observation: since 1955, U.S. construction costs have moved in only one direction. The Turner Construction Cost Index has continued to confirm that pattern — costs rose meaningfully in both 2024 and 2025, with the steepest increases in materials exposed to tariff and supply-chain volatility.

Property insurance has compounded the pressure. According to Marsh's 2025 Insurance Market Report, commercial property premiums rose between 8% and 25% in catastrophe-exposed regions through 2025. Lenders are now treating insurance review as a standalone underwriting workstream rather than a closing-week formality.

On rate forecasting, an MBA CREF 24 panelist captured the discipline well: "Rates only began rising about seven quarters ago, after nearly four years sub-two percent. Maybe we've just been spoiled all this time." That recalibration of expectations turned out to be the right operating frame — long rates remain rangebound near 4%, well above the 2018–2021 baseline.

Adapting Real Estate Strategies with Creative Capital Solutions

MBA CREF 24 panelists were direct: lending in today's CRE market — particularly in affordable housing — is structurally more complex than it was pre-2022. Capital deployment now relies on a layered toolkit, not a single debt-and-equity stack.

The creative capital solutions surfaced at the conference, and now mainstream in 2026 underwriting

• Public-Private Partnerships (PPPs): share financial risk and reward between public agencies and private investors; support projects that fail traditional financing screens.

• Low-Income Housing Tax Credits (LIHTC): the dominant equity source for affordable housing; per HUD, LIHTC has financed over 3.7 million affordable units since 1986.

• Green Bonds: issued for environmentally sustainable projects; 2025 was a record year for green bond issuance in CRE, per Climate Bonds Initiative.

• Crowdfunding Platforms: aggregate retail capital for larger deals — useful for sponsors below institutional scale

• Flexible Loan Structures: adaptable terms tied to project milestones and timing; increasingly common as lenders price for more risk scenarios.

• Opportunity Zone Funds: tax-advantaged investment in designated areas; reauthorized into 2026 with refined eligibility rules.

• Mezzanine Financing: fills the gap between senior debt and equity; per CREFC data, mezzanine origination volume rose materially in 2024–2025 as senior LTVs tightened.

• Joint Ventures: share strengths and resources across parties; the dominant structure for value-add and development deals in 2026.

• Land Leases: lower upfront land costs by leasing rather than buying; freeing capital for construction and lease-up reserves.

PRACTICAL TAKEAWAY

In 2026, the right capital stack is a multi-instrument question. Run senior, mezzanine, agency, and JV scenarios in parallel — not sequentially — when pricing a deal. The cheapest source of capital may not be available at the credit profile the deal actually carries.

Smart Capital Center: Transforming Mortgage Transactions in a Volatile Market

MBA CREF 24's central message — that maturities, inflation, rate volatility, and construction-cost pressure would force a faster, data-richer operating model — has played out. Smart Capital Center supports that operating model directly. The platform analyzes 1B+ real-time data points across 120M+ properties, with $500B+ in CRE transactions already analyzed for clients including KeyBank, JLL, The RMR Group, Community Preservation Corporation, Aareal Bank, and Tremont Realty Capital.

Ken Schroeder, KeyBank: "SCC reduced our financial model prep time by 40%. What used to take three analysts a full day now takes one analyst two hours — with cleaner outputs and full traceability for our loan committee."

Fernando Salazar, JLL: Reports a 30x productivity gain on specific underwriting workflows after embedding SCC across the team.

The platform compresses the full mortgage transaction lifecycle — origination, screening, underwriting, asset management, servicing, and disposition — into a single workflow. For lenders confronting the 2026 maturity wall, that compression is the difference between answering the loan committee's questions in hours rather than days.

Wrap Up

MBA CREF 24 framed the questions that have defined CRE finance through 2026: the maturity wave, sticky-but-moderating inflation, a steeper yield curve, persistent construction-cost pressure, and the operational case for technology-led underwriting. The 2026 data has answered most of them.

The bottom line: $875 billion in CRE loans mature in 2026, originations are projected to grow 27% to $805 billion, and the lenders and investors who can underwrite faster and price risk more accurately will set the terms for the next cycle. Smart Capital Center is built for that operating tempo.

Frequently Asked Questions

How much commercial real estate debt actually matures in 2026?

$875 billion, or 17% of the $5 trillion in outstanding U.S. commercial mortgages, according to the MBA's 2025 CRE Survey of Loan Maturity Volumes. That figure is 9% lower than the $957 billion that matured in 2025 but still roughly 2.5x the 20-year average. Bank-held loans account for the largest single concentration at $396 billion.

Which property types face the most refinancing pressure in 2026?

Office is the most exposed sector — CMBS office delinquency hit 7.29% in Q2 2025 (Federal Reserve and Kaplan Group data). Multifamily and industrial remain the strongest, with abundant agency liquidity supporting refinance activity. Healthcare and life sciences are also stable on demographic tailwinds, with reduced 2026 construction completions supporting vacancy.

What did MBA CREF 24 predict, and how did those predictions hold up?

The 2024 conference predicted a sustained refinancing wave, near-term rate cuts paired with rangebound long yields, moderating shelter inflation, persistent construction-cost pressure, and growing demand for workforce-housing structures. All five predictions have largely played out — making the conference's framing the right operating lens for the 2026 cycle.

Will the Federal Reserve cut rates again in 2026?

Most forecasters expect one to two additional cuts. CBRE's 2026 outlook is built around long-term yields stabilizing near 4%, with most cap rates compressing 5 to 15 basis points as a result (CBRE, 2026). The MBA expects originations to grow 27% on the back of that environment.

What is the difference between a loan extension and a refinance?

A loan extension keeps the original debt structure in place and pushes the maturity date. A refinance replaces the existing loan with a new instrument, typically with revised pricing, term, and covenants. Many 2024 and 2025 maturities were extended rather than refinanced — which is why 2026 maturity volume remains elevated relative to historical averages.

How is AI changing CRE underwriting in 2026?

AI is compressing the underwriting cycle from days to hours by automating data ingestion, comp-set construction, sensitivity analysis, and covenant tracking. Smart Capital Center analyzes 1B+ real-time data points and has supported $500B+ in transactions. Clients including JLL report 30x productivity gains on specific workflows, and KeyBank reports a 40% reduction in financial model prep time.

How do I prepare a portfolio for the 2026 maturity wall?

Run a portfolio-wide DSCR stress test at +200 and +350 basis points, refresh valuations on every asset over $5 million, identify modified loans that will drop off regulatory reporting, and confirm insurance coverage adequacy on every collateral position. Most credit committees are now running this review quarterly, not annually.

UNDERWRITE THE 2026 MATURITY WALL

1B+ live data points behind every refinancing decision. 50% faster deal execution. 360° real-time risk and market analysis.

.png)